60 days to go before I pull the plug – are we getting closer with our financial goals?

January brought some relief with markets becoming more optimistic in the new year:

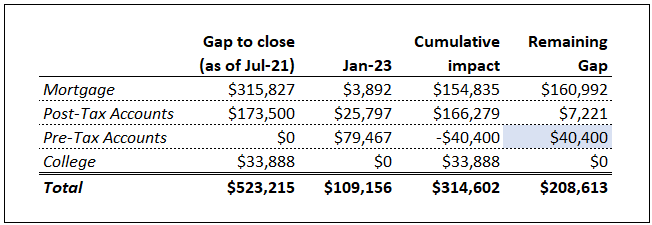

The gap to close shows what we need to accomplish by May 2023 to be able to retire early. In January we “gained” $109K, which made the cumulative impact of $314.6K, with $208K to go… But most of the remaining gap is in Mortgage, which I would be ok with if we don’t pay it down fully before the retirement, and I would rather build out the cash cushion for the first 1-1.5 years of retirement. We are still retiring in April (or rather, I am, as I am not sure about my husband at this point. He is considering working till July or maybe even till December!), and I believe the market will turn around in 2023/2024 and will help us close the gap fully!

Mortgage

This is the largest item in the table above. We want to retire without any debt, and the vacation house mortgage is the last debt item we have.

As of July 2021, we had $315,827 in principal due to the bank. In January we contributed $3.9K towards closing the gap. I continue saving money as cash instead of paying extra mortgage (for now) to build enough emergency funds to cover us through 1.5 years since the market is doing what it is doing these days…

Cumulatively, since July 2021 we reduced the mortgage gap by $155K, 49% of the gap. I am still pursuing the current intent to build a sizeable cash reserve rather than aggressively pay down the remaining mortgage, so I don’t anticipate that we close the mortgage gap comes April 2023. I anticipate having about $149K left, which we can pay down on the normal remaining schedule over the next five years. If some time in the next year or two the stock markets soars, I would be happy to pay it out with the appreciated stocks. As of now, that’s not such a high priority for me.

Post-tax accounts

Post-Tax accounts include cash and stock we own in our Brokerage Fidelity accounts. They also include the value of contributions I am making towards ESPP purchases.

In January, the value of our post-tax accounts increased by $25.8K, thanks to the market performance. Again, I am piling some cash, so that I don’t have to sell stocks while in recession, which may still happen during 2023. Next month I am expecting a bump due to my annual bonus and some RSUs vesting.

Pre-tax accounts

Pre-tax accounts include 401K plans with our current employers and Traditional IRAs.

In January, the value of our pre-tax accounts has increased by $79.5K, not fully offsetting the paper losses during last year but bringing us closer to “no change whatsoever in our pre-tax accounts” – have another $40K to offset 🙂 . I am still not worried about theoretical losses in the pre-tax accounts – we won’t be able to use these money for at least five years, which means I am very certain that by the time we get to use that money there will be a significant growth in those accounts. Besides, if the stocks are still depressed when we start doing Roth IRA conversions, we’ll have to pay fewer taxes on the conversion with the stocks being valued lower.

Conclusion

In summary, 2022 started well on the investment front. Hoping that the worst is over and that we’ll start seeing some growth in our investments. With only two months to go, we continue contributing to our pre- and post-tax accounts, but with the main focus on building cash reserve with the only stock purchases through the tax savings and discount programs, such as 401K contributions and ESPP purchases… I am positive that we’ll be in a good place closer to the retirement date! I have to be!

Stay tuned to the future updates!