Ok, the time for the next financial update – what progress has been made towards achieving Early Retirement?

February turned out to be a crazy month, for multiple reasons… Russia started a war with Ukraine, our son decided to withdraw from college… The markets had been up and down, and even my annual bonus did not push us into a positive territory…

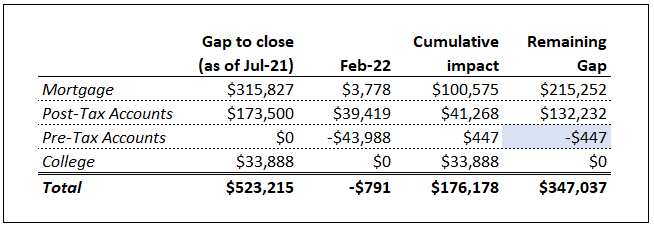

The gap to close shows what we need to accomplish by May 2023 to be able to retire early. While we are making progress in some areas, we are losing in others… By the way, due to my son withdrawing from college, I decided to re-direct the remaining unpaid college goal into Post-Tax accounts, which is why the total gap to close stayed the same, but the Post-Tax Accounts gap was increased and College gap was tapped at what we already paid for the two quarters of studying.

Mortgage

This is the largest item in the table above. We want to retire without any debt, and the vacation house mortgage is the last debt item we have.

As of July 2021, we had $315,827 in principal due to the bank. In February we continued contributing $3,780 towards closing the gap. We weren’t able to put away additional $3.5K (as I would normally do) because we had to pay a large tax bill on all properties, which happens every six months. Plus I decided to diversify our holdings by buying some I-Bonds, which are adjusted for inflation and currently have a yield of 7.12%, way better than the 2.5% we would have saved if I paid down the mortgage. See more on that below.

Cumulatively, since July 2021 we reduced the mortgage gap by $100.6K, 34% of the gap.

Post-tax accounts

Post-Tax accounts include cash and stock we own in our Brokerage Fidelity accounts. They also include the value of contributions I am making towards ESPP purchases.

As I mentioned before, by redirecting the remaining College funds I increased the gap to close from $102K to $173.5K by May 2023. In February, because of my annual bonus, we contributed the usual $8.6K in ESPP. We also purchased $20K worth of I-Bonds, to have a hedge against the inflation. Current annualized yield on the I-Bonds is 7.12%, and while it will change in May for the next six months, it will be at least the level of inflation, which I don’t expect to drop in the near future due to the ongoing political climate. We also transferred $4K into the brokerage accounts so that DH could hone his trading skills buying and selling a single share of Amazon 🙂 And one more thing: I had a portion of my Restricted Stock Unit options (RSU) vested, total of 68 shares of my company at $115 each, so the value of the vested RSUs is about $7.2K. All of those additions boosted our Post-tax accounts and contributed $39.4K to the closure of the gap in February without any contributions from Mr. Market.

Pre-tax accounts

Pre-tax accounts include 401K plans with our current employers and Traditional IRAs.

In February our pre-tax accounts have decreased by $44K, cancelling any progress we made since July. So as of now we have about $0 gains in our pre-tax accounts, for which we did not plan anyways, so we are still on track.

College costs

We planned to cash flow the first two years of college for our eldest son, who just started college in this year. However, this month he decided to withdraw from college, which negated the need to close that specific gap.

We paid about $34K for educational expenses so far, but from now I will stop tracking that category of expense. Sigh.. We’ll see what the future will bring.

Conclusion

In summary, February was not a mixed month for us, resulting in a wash. We made some progress in post tax accounts and mortgage category but lost whatever windfall we had in pre-tax accounts. At this point, we closed the gap by $176K. That represents about 34% of the gap we need to close. We continue to chip away at our financial goals and hope that the market cooperates in the next couple of years! Markets can go up or down, we will still reach our goal 🙂

Stay tuned to the future updates!

Good day! I just wish to give you a huge thumbs up for your excellent information you have got here on this post. I am coming back to your blog for more soon.

Thank you! I appreciate your comment and hope to provide more interesting content in the future 🙂