Ok, the time for the next financial update – what progress has been made towards achieving Early Retirement?

December had been an awesome month for us financially! Three pay periods, a large semi-annual bonus and market growth resulted in a great progress towards our early retirement goals!

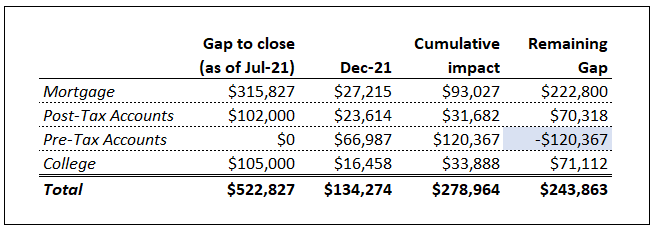

The gap to close shows what we need to accomplish by May 2023 to be able to retire early. As you can see, due to the factors listed above, the net contribution in December was $134K.

Mortgage

This is the largest item in the table above. We want to retire without any debt, and the vacation house mortgage is the last debt item we have.

As of July 2021, we had $315,827 in principal due to the bank. In December we were able to put $27,315 towards closing the gap (amazing semi-annual bonus, I know!). Cumulatively, since July 2021 we reduced the mortgage gap by $93K, 29% in six months.

Post-tax accounts

Post-Tax accounts include cash and stock we own in our Brokerage Fidelity accounts. They also include the value of contributions I am making towards ESPP purchases.

As of July 2021, we needed to add another $102K by May 2023. In December post-tax accounts increased by $23.6K, most of which was due to market growth (ESPP contributions added $2.7K). Currently, we closed 31% of the original gap in six months.

Pre-tax accounts

Pre-tax accounts include 401K plans with our current employers and Traditional IRAs.

Note that the gap to close for post-tax accounts was $0. That’s right, we already have enough funds in the tax-advantaged accounts and don’t need to actively grow them as much. However, we continue maxing out our 401K contributions to reduce taxes and to take advantage of company’s match.

In December our pre-tax accounts have increased by $67K, more than double the loss we experienced last month. So as of now we have $120K more in our pre-tax accounts than we originally planned, a nice add-on towards the early retirement 🙂

College costs

We need to cash flow the first two years of college for our eldest son, who just started college in this year.

In December we made the second payment in the amount of $16.5K. The next payment is expected in March, before the beginning of the last quarter of the school year.

Conclusion

In summary, December more than made of for the disappointing November performance, resulting in nice progress towards our goals. At this point, we closed the gap by $158.5K, not counting the unexpected windfall in pre-tax accounts, which is an icing on the cake. That represents about 30% of the gap we need to close. We continue to chip away at our financial goals and hope that the market cooperates in the next couple of years!

Stay tuned to the future updates!