Ok, the time for the first financial update – what progress has been made towards achieving Early Retirement?

July was a great month to make a progress. Dear Husband (DH) received his semi-annual bonus, which went a long way towards closing the gap between where we are today and the prospect of retiring early in 2023. We also received three bi-weekly paychecks (that happens twice a year, since there are 12 months in a year and 26 paychecks).

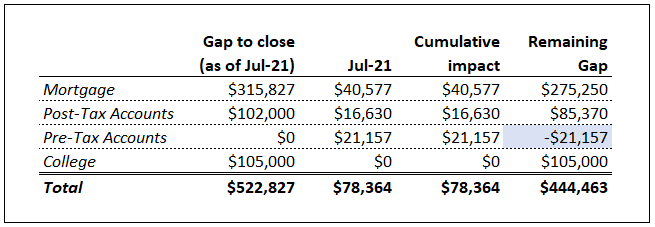

The gap to close shows what we need to accomplish by May 2023 to be able to retire early. Obviously, this is not ALL the resources we have, but closing the gap above will be the final stretch to round up our financial situation and provide us with the piece of mind needed for the early retirement.

Mortgage

This is the largest item in the table above. We want to retire without any debt, and the vacation house mortgage is the last debt item we have.

As of July 2021, we had $315,827 in principal due to the bank. Due to the generous semi-annual bonus, we were able to reduce the amount by $40,577. Not every month will be so great, but July was one of those months…

Post-tax accounts

Post-Tax accounts include cash and stock we own in our Brokerage Fidelity accounts. They also include the value of contributions I am making towards ESPP purchases (the money is being taken from of my paychecks and accumulated in a separate account, out of which twice a year my company’s shares are purchased at 15% discount and then placed into my brokerage account).

As of July 2021, we needed to add another $102K by May 2023. In July post-tax accounts increased by $16,630. While ESPP contributions increased by $2,790, the rest of growth was driven by market.

Pre-tax accounts

Pre-tax accounts include 401K plans with our current employers and Traditional IRAs, into which we converted our previous employers’ 401K plans.

Note that the gap to close for post-tax accounts was $0. That’s right, we already have enough funds in the tax-advantaged accounts and don’t need to actively grow them as much. However, we continue maxing out our 401K contributions to reduce taxes and to take advantage of company’s match.

In July our pre-tax accounts have grown by $21,157, $8,470 of which were 401K contributions/employers’ match, and the rest – market growth.

College costs

We need to cash flow the first two years of college for our eldest son, who just started college in this year. Since the chosen college is out of state and our income is high, unfortunately, the college costs are also high, even with receiving some scholarship.

The college starts in the fall, so the payments for college will start in August/September. I will provide an update next time.

Conclusion

In summary, July was a great month, and market growth, in addition to an amazing semi-annual bonus and three paychecks helped make a sizeable dent in the gap that we need to close. I am hopeful that we’ll meet our goal before May 2023!

Stay tuned to the future updates!