Ok, the time for the next financial update – what progress has been made towards achieving Early Retirement?

As we are getting closer to our finish line, the equilibristic of the markets is driving me nuts! Where is the stability, I am asking you? 🙂 After such a nice rally in July, August turned around and lost all the gains from the previous month! Well, maybe not all, but you know what I mean, right? Feels like two steps forward, one step back… Let’s dance, the stock market, let’s dance!

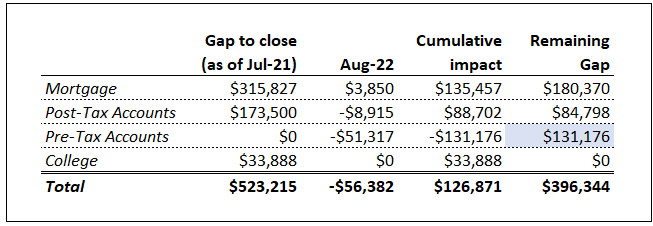

The gap to close shows what we need to accomplish by May 2023 to be able to retire early. With the latest market performance, the gap to close shrank (grew?) to $396K, which is much better that what we’ve seen at the end of June but it’s a slight step back (if you can call $56K theoretical loss a slight step back).

Mortgage

This is the largest item in the table above. We want to retire without any debt, and the vacation house mortgage is the last debt item we have.

As of July 2021, we had $315,827 in principal due to the bank. In July we contributed $3.8K towards closing the gap. This month we did not contribute additional $5K towards the principal, because with markets being down, I am thinking about investing more into stock markets (buying the dip).

Cumulatively, since July 2021 we reduced the mortgage gap by $134.5K, 43% of the gap. Since we have less than a year to go before we pull the plug, the question is – are we going to meet this goal by May 2023? I think we still can but even if we don’t, with the amount that will remain (I definitely think it will be less than $100K), we can cash flow the remaining mortgage over the next couple of years. Or, if the stocks appreciate well enough in the next year or so, selling some extra stocks from the brokerage account may be an option to just close that gap.

The reason we are not as aggressive with the mortgage payments as originally planned is that now that the markets are down, I believe it’s better to invest free money into stock market (buying at the discount) than to get the “guaranteed return” of 2.5% of mortgage interest. If I am right, then the money invested in the stock market will result in enough funds to pay down the mortgage plus some additional growth that will pad our brokerage accounts and make the next few years sailing smoother. That will happen sooner (next year) or later (in the next couple of years). Either way, I think it’s a better investment right now.

Post-tax accounts

Post-Tax accounts include cash and stock we own in our Brokerage Fidelity accounts. They also include the value of contributions I am making towards ESPP purchases.

In August, the value of our post-tax accounts declined by $10K, driven by the market declines. In August we did not make any investments but set aside cash for the potential project.

Pre-tax accounts

Pre-tax accounts include 401K plans with our current employers and Traditional IRAs.

In August, the value of our pre-tax accounts have declined by $51K, losing half of the gains from the previous month. On the other hand, I am not so worried about theoretical losses in the pre-tax accounts – we won’t be able to use these money for at least five years, which means I am very certain by the time we get to use that money, there will be a significant growth in those accounts.

Conclusion

In summary, the market rollercoaster continues. Declines in February, gains in March, declines in April/May/June, gains in July, and now losses in August. We continue contributing to our pre- and post-tax accounts, knowing that eventually the market will go up, just not sure when… After a whole year, we closed the gap by $127K but if/when the market fully recovers, we should see a much bigger progress towards our goals. For now this represents about 24% of the total gap we need to close, but if I were to exclude pre-tax accounts, my gap is closed by 50%, which is much more realistic view at my finances right now ;). I am still positive that we’ll be in a much better place closer to the retirement date!

Stay tuned to the future updates!