Ok, the time for the next financial update – what progress has been made towards achieving Early Retirement?

Another one of those months when the market kept going down and up and down again… Since we can’t control the market, the only thing we can do in this situation is to continue contributing to the accounts, paying down the mortgage and hope that the market eventually cooperates 🙂

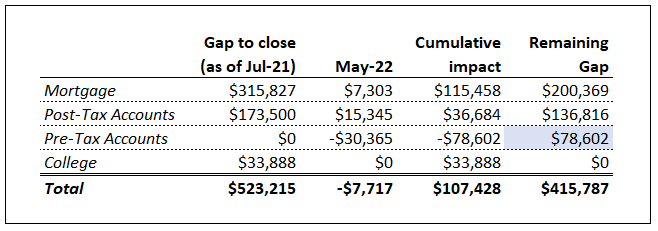

The gap to close shows what we need to accomplish by May 2023 to be able to retire early. Altogether, due to market declines, we continued seeing some losses (though not as large as what we’ve seen in April). Kind of a neutral month, with some negative aftertaste…

Mortgage

This is the largest item in the table above. We want to retire without any debt, and the vacation house mortgage is the last debt item we have.

As of July 2021, we had $315,827 in principal due to the bank. In May we continued contributing $7.3K towards closing the gap. This month we restarted putting away additional $3.5K towards the principal, now that we paid property taxes for our house and the condo.

Cumulatively, since July 2021 we reduced the mortgage gap by $115.5K, 37% of the gap. This is the only goal that is not dependent on market fancies, the gap just continues closing, and that’s the most important piece of the puzzle right now.

Post-tax accounts

Post-Tax accounts include cash and stock we own in our Brokerage Fidelity accounts. They also include the value of contributions I am making towards ESPP purchases.

In May, the value of our post-tax accounts increased by $15.3K, most likely due to the increase in value of my company’s stocks and vesting of a third of the additional bonus that was granted to me last May.

Pre-tax accounts

Pre-tax accounts include 401K plans with our current employers and Traditional IRAs.

In Maythe value of our pre-tax accounts have declined by another $30K, despite our regular contributions of about $4K in 401K (including the employer’s match). I guess the market forces are stronger than our contributions 🙂

Conclusion

In summary, the market rollercoaster continues. Declines in February, gains in March, now declines in April, continued declines in May. We continue contributing to our pre- and post-tax accounts, knowing that eventually the market will go up, just not sure when… At this point, we closed the gap by $107K (another step back from the highs we’ve seen at the end of last year). That represents about 21% of the gap we need to close. We continue to chip away at our financial goals and hope that the market cooperates in the next couple of years! Markets can go up or down, we will still reach our goal 🙂

Stay tuned to the future updates!